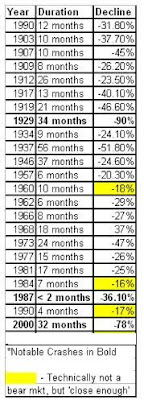

"Technical analysis, the prediction of price movements based on past price movements, has been shown to generate statistically significant profits despite its incompatibility with most economists' notions of "efficient markets." Federal Reserve Bank of New York, C.L. Osler and P.H. Kevin Chang, Staff Report No. 4, August 1995.)

Support and Resistance are among the most basic forms of technical or chart analysis. I felt that this would be a good topic to cover today since support played an important role in the recent market downturn that happened last week. Many stocks that PMC tracks had long term support break down last Thursday or Friday. I'm going to focus on one of those stocks for this article.

This is a daily candlestick chart of Google Inc. from March 2009 until January 22, 2010. Please click on the image to see the entire chart.

This is called a candlestick chart. The red candles represent down days and the green candles represent up days. The bottom white line I have drawn represents where the support of the stock is. Support means that the stock is not likely to break below that area unless there is some change in sentiment. The support exists because there is sufficient buying demand at these levels to overcome selling pressure. The upper line represents where resistance is in the stock. This is where the stock is unlikely to break above unless there is some sort of change in people's opinion of the stock. This is the point where selling pressure overcomes the buyers of the stock. When the support and resistance are both trending upwards in this fashion, it is called an ascending channel. Each time the stock bounces off of the support or resistance traders notice, it reconfirms the support, and makes them all that much more difficult to break out of the next time.

You may ask, why does the stock haves support and resistance? Likely, some of it has to do with self-fulfilling prophecy. Humans are pattern recognition machines. When many people see the same pattern in the stock chart they may react in the same way. There are other reasons such as automated trading programs utilized at large institutions, people's propensity to focus on even numbers, or any other number of reasons. Ultimately, it doesn't really matter why it works just as long as it does.

As you can see in the above chart, Google stayed in its channel for nearly eleven months. There are a few different strategies that could have been successfully employed with Google over this time period. Since the channel was ascending, the most logical strategy would have been to purchase the stock in March or after the support had been confirmed and held onto it until the support level was broken on January 22nd.

So why after 11 months did Google drop below its support level (as shown in the circled portion of the chart)? On January 21, 2010, Google reported their quarterly results and the market reacted poorly to the news. The quarter's results changed the investors sentiments about the stock and thus there were no longer enough buyers at the support level to keep the stock elevated to that level. When a stock breaks below a major support level, often they fall to the next major support level. Major moving averages of a stock are often seen as support levels for stocks. The yellow line on the chart represents the stock's 100-day moving average. Once traders saw that Google had breached its previous support level, there was a high probability of the price falling to a major moving average. The 100-day happened to be the closest to the support level, and so one could have shorted the stock until the price reached the 100-day moving average and then covered their short with a relatively high probability of success. As you can see, Google closed almost exactly on the 100-day moving average.

Before investing in stocks, we recommend looking at both longer term and short term charts to determine where major support and resistance levels exist for a stock. Generally, it is not wise to buy a stock near its resistance level. On the other hand, buying near a major support level can give you some confidence that you bought the stock for a good price. However, nothing is certain. Many people bought Google on January 20th assuming that it would move back up after hitting its resistance level, but unluckily for them, this happened to be the time that the stock broke down below its support because of the change in the sentiment of the stock.